Liberty offers a 401(k) plan managed by Fidelity Investments. An employee is eligible to participate in the Company 401(k) Plan immediately upon hire if they are at least 20 years old. Eligible employees will be automatically enrolled at a 2.0% salary deferral unless they contact Fidelity Investments to change or stop the deferral. Employees will have 30 days to opt out or change this deferral amount before it becomes effective.

Employees will also have the option of deferring post-tax salary to a Roth plan. Deferral amounts made to this plan are eligible for the employer match. Note – The Roth plan is not subject to the autoenrollment feature and requires an active deferral election initiated by the plan participant.

The current employer match is 35% on the first 4.0% of salary deferred, to the 401k or Roth plan (combined). Employees must work for any Liberty entity for at least one year to begin earning the company match

Former employees who are rehired or new employees hired through acquisition will retain their original date of hire with the acquired location to determine company match eligibility and for vesting purposes.

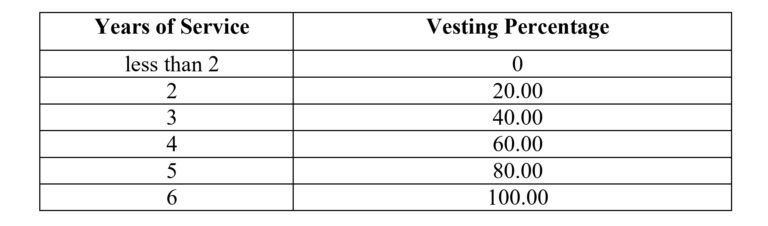

Vesting Schedule

If you terminate your employment, you may be able to receive a portion or all of your Account based on your vested percentage. You are always 100% vested in your Rollover Contributions, Qualified Non-elective Contributions, Deferral Contributions and any earnings thereon. Your Employer Matching Contributions and any earnings thereon will be vested in accordance with the following schedule:

Rollovers

Participants may roll over part or all of an eligible rollover distribution received from an eligible retirement plan. An eligible retirement plan is a qualified plan under Section 401(a), a 403(a) annuity plan, a 403(b) annuity contract, an eligible 457(b) plan maintained by a governmental employer, and an individual retirement Account and individual retirement annuity.

The Plan will accept direct Rollover Contributions of amounts attributable to Roth contributions made to another qualified plan that accepted Roth Deferral Contributions and properly segregated them from other contributions.